Black Swan? Hardly! Revolutions and Tsunamis Come and Go!

By Ann Grackin

Published

on Apr 5, 2011

Unpredictability of events misses the point in Risk Management.

Full Article Below -

Untitled Document

Firstly, I want to state that I am a big fan of Nassim Nicholas Taleb (left), the author of Black Swan. If you have not read this—you should. It is fundamental to understanding markets. (Besides his two books, he shares many of his ideas on his website.)

Creating a resilient enterprise is critical to customer protection and employee welfare, as well as securing the financial viability of the company. Yet many firms think that since rare events are unpredictable, then there is no sense in doing much about them other than “risk transfer” (purchasing a risk product, if one is available, such as product liability, property and casualty and so on).

2011 has already brought us big tragedies: Middle East revolts, which have now turned quite violent, impacting the cost of commodities; and the Japanese tsunami, impacting trade and financial markets. Human tragedy aside, many risk professionals take the approach that since the where and when of these types of events are not predictable, there seems to be no point in planning ahead with business continuity plans, and methods—both process and analytical—to understand, avoid, or at least respond quickly and smartly, lessening their impact.

So let’s get back to Taleb. He talks about the high impact of rare events:

“We don't understand the world as well as we think we do and tend to be fooled by false patterns, mistake luck for skills (the fooled by randomness effect), overestimate knowledge about rare events (Black Swans), as well as human understanding, something that has been getting worse with the increase in complexity.”

A few pointers here. If we think back to 9-11, everyone came to the conclusion that we were impacted mostly due to a failure to imagine. We were sitting on the information. This was the same in Japan. Could we not have imagined a 9.0 earthquake instead of a 7.5? Or, in the case of Katrina, could we not have imagined a few more feet of water? A 5.0 hurricane instead of a 4.5? Why not? Taleb’s premise is that the modelers and forecasters look through a faulty lens; they discount these events because they are rare:

“We learn from crisis to crisis that modern financial theory has the empirical and scientific validity of astrology (without the aesthetics); yet thelessons are forgotten and ignored in what is taught to 150,000 business school students worldwide.”1

His position in the current Japanese nuclear situation, I think, is this: these events are forecastable, so we ought to include, not exclude them in our forecasts. There is too much at stake not to.

Being in the research field, I find it very easy to see how statistics and forecasting fail to miss what might, in hindsight, have seemed obvious. Overreliance on mathematical models can lead to strange theories (string theory of the universe) or myopia, such as with this tsunami. Many forecast models justify what you already know instead of using various fresh data sources and challenging your model. They fail to ask, “What if?”

Having spent some time in the risk industry,2 I learned that smart risk modeling asks questions differently:

Stretch the range of the model (to 9.0 or 10.0)—what would it look like?

But more importantly, what would the impact be? How would I recover from the impact?

Obviously, if you are in the insurance business, you want to know, “What’s this going to cost to recover?”

Notice that I did not state as the top question, “What is the probability of an event?” Yes, you need to ask that, too. But if you focus on the events vs. the impacts, you get hung up on the probability of a single event vs. the cluster of various events and their impacts.

Where to begin?

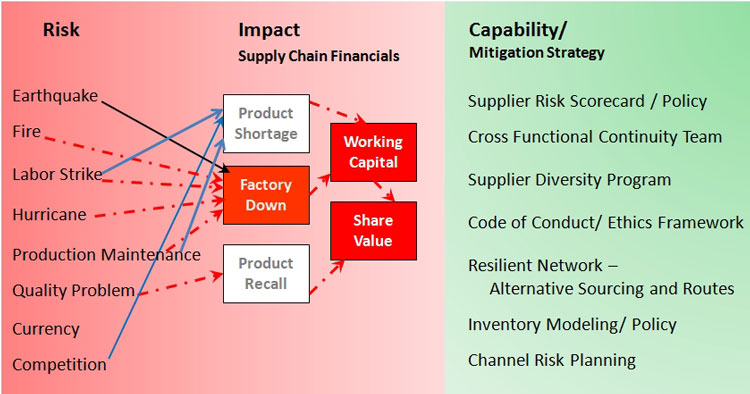

Let’s take Company X. They have customers and plants throughout the world. Their plants feed parts to each other. They also have suppliers hither and yon. Some of these suppliers provide material that is often scarce. Impacts by weather, production quality, or demand variability are merely a few causes for scarcity. A prime example would be a plant on a fault line in an area that has intermittent power outages. Figure 1 shows the limitation of focusing solely on the probability of a causal.

Figure 1 - Impact / Capability

The causal could be anything. It may be unlikely that we get a hurricane. But what about a power outage or fire? Something awful could happen. Which one, we just don’t know. And that is where so many conversations in business break down. If it is unlikely to happen, let’s move on to other priorities. No time, no money to spend on this. However, as we have learned from many events, firms can be equally impacted by internal causes—labor strikes or production problems, as well as external—weather, politics, etc.

Companies build processes that are surprisingly, obviously vulnerable, regardless of cause.

In addition, certain events have secondary impacts. The scale and impact of one event can be a tipping point to many secondary effects, such as the tsunami leading to the nuclear crisis.

So, we need to understand and build into our models that something will go wrong. Regardless of cause, is this process vulnerable? Having ‘one source’ for data, for supplies, for expert labor, or for cash are just such examples. Being in a poor cash position as an organization or government also qualifies as vulnerability. Regardless of cause, the impact may be the same.

Though recovery activities from a fire may be different from those of a labor strike, the impact is that your factory is closed. These have primary and secondary impacts such as having to buy product on the open market to fulfill demand (impacting working capital, affecting profits, and reducing shareholder value).

Catastrophic Events

But what if the event impacts the whole nation or the whole industry sector? Isn’t that different? If all my competitors are in the same situation, why should I invest more on risk programs?

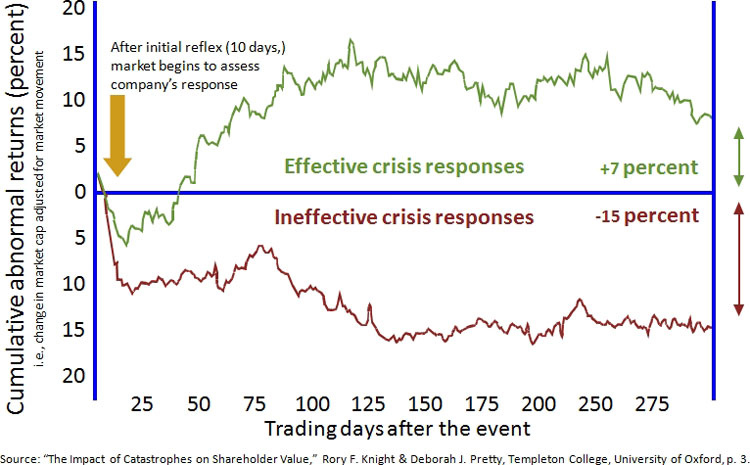

Figure 2 - Impact on Sharholder Value

I talked to Lisa Grossman, Vice President of ImpactFactor, a supply chain risk and analytics firm. Ms. Grossman has a background in financial modeling, working with hedge funds in NYC before co-founding ImpactFactor.

She tracks many manufacturing sectors to see how their financial performance and share price is impacted by supply chain volatility:

“When high impact events occur that affect a whole geographic or industry sector, clearly, the sector will be impacted. But not all companies are impacted the same.”

Here was an insight that I think many of us don’t think much about (again, in a big event like a dock strike, everyone will be impacted the same, right?) As you can also see in Figure 2, Knight and Pretty of the University of Oxford modeled the impact and recovery of shareholder value of companies with continuity plans vs. those without. Those with effective continuity plans recovered more quickly.

Ms. Grossman goes on to point out,

“After the initial event, companies recover at different rates—if at all. Well managed companies, who have financial and supply chain reserves, will recover some if not all of their market value, relatively quickly. Those that don’t have a strong working capital foundation, as well as effective continuity plans, won’t bounce back.”

In addition, the purely prepared can sell when others can’t. The ability to understand and track supplies, for example, was deftly demonstrated in the dog food crisis. One brand was able to track, and to demonstrate to the public that they had safe food. So while all the other brands were swept from the shelves, they captured market share! You often can monetize preparedness.

ChainLink also saw in our demand management/supply chain studies that firms that had good data on their demand and consumption and had collaborative relationships with their suppliers had a much better handle on where they stood when various events occured.

My take away is this: You can’t prevent a specific event, but you can be prepared for a variety of events or outcomes. As our grandparents told us, ”Save for a rainy day.”

Conclusions:

Crying out “Black Swans” may be chic, but many of those who do may not understand Mr. Taleb. He challenges the notion that these are random and therefore unpredictable events, so we can’t plan and predict better to avoid being impacted. His perspective is that they are not as random as you think and that a lot of common sense—and evidence in plain sight—would lead people to more enlightened behaviors and preventions.

My long-term thought is that obsession with the competition and the (almost) useless activities such as benchmarking will lead us to inaction—passivity. If my competitor is not doing this, why should I?

Passivity in the face of such challenges is sadder than the events. But if we do not learn from them—that is a true tragedy.

1 Excerpt from History Written by Losers, by NASSIM NICHOLAS TALEB 2 While I was employed at Marsh & McLennan, which took my understanding of risk management to a much deeper level.

To view other articles from this issue of the brief, click here.

Firstly, I want to state that I am a big fan of Nassim Nicholas Taleb (left), the author of Black Swan. If you have not read this—you should. It is fundamental to understanding markets. (Besides his two books, he shares many of his ideas on his

Firstly, I want to state that I am a big fan of Nassim Nicholas Taleb (left), the author of Black Swan. If you have not read this—you should. It is fundamental to understanding markets. (Besides his two books, he shares many of his ideas on his